State of Salmon Aquaculture Technologies, 2019

On this page

- Executive summary

- 1 Introduction

- 2 Scope of assessment

- 3 Sustainable aquaculture technology criteria

- 4 New technology assessment

- 5 Development pathway in British Columbia

- 6 Bibliography

Executive summary

Purpose

There is strong interest from government, industry, non-government organizations and Indigenous peoples to accelerate the adoption of salmon aquaculture technology that minimizes environmental impacts in British Columbia, while supporting rural economic development, employment, and the security of Canada’s food supply.

Background

Globally, there are two primary drivers of new salmon production technologies, namely:

- pressures from governments and stakeholders to adopt more environmentally friendly technologies

- challenges such as sea lice and algal blooms that affect salmon production. The industry has largely focused on improvements to conventional marine netpen systems to improve environmental performance while maintaining operational and financial feasibility, but new alternative production system technologies are advancing to meet these needs.

Indigenous communities

Indigenous communities have a key role to play as they already contribute at least 10% of Canada’s aquaculture economic activity and are engaged in every aspect of the salmon farming value chain. They have played a central role in new technology developments including the Kuterra land-based RAS project. Furthermore, the Government of British Columbia adopted a policy in 2018 whereby, starting in 2022, the Province will grant tenures only to fish farm operators who have negotiated agreements with the First Nation(s) in whose territory they propose to operate.

Approach and scope

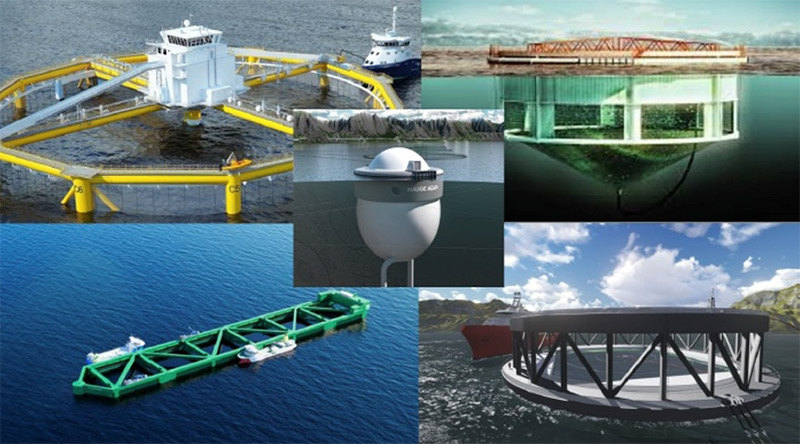

This report highlights Canadian developments along with a global scan of major technological advancements in four production systems that offer new opportunities for producing market-sized salmon:

- land-based recirculating aquaculture systems (RAS)

- hybrids involving land and marine based systems

- floating closed-containment systems (CCS)

- offshore open production systems

Other technologies that support the main production systems are discussed including: sensors and control systems, data analysis for “intelligent farming”, feed innovation, transport and logistics, nets and mooring, robotics, and broodstock development.

State of development

The current global status of the four production technologies is described briefly to illustrate key features, current production capabilities, indications of planned and actual commercial scale operations, key requirements for successful deployment of each system, and on-going areas of research that aim to address remaining challenges.

British Columbia meeting requirements

There are valuable assets in B.C. that serve as a foundation for developing these technologies including: the well-developed aquaculture industry with transferable expertise, research and training capabilities, fish health and diagnostic capacity, supply chain inputs such as feed sources and distribution of products to markets, as well as the biophysical advantages of coastal B.C. More specific site requirements such as saltwater and freshwater resources, access to low carbon grid-connected power, road and communication networks, waste discharge and processing options are also discussed. Overall, B.C. is well-positioned for existing salmon farmers and new industry entrants to successfully develop these technologies.

Assessment of strengths, weaknesses, and uncertainties

The four production systems are evaluated across seven (7) environmental criteria, three (3) social criteria, and seven (7) economic criteria. These represent key requirements that must be met for salmon production volumes in B.C. to resume historic growth trends. The assessment reflects the broad state of technologies rather than specific designs, and uncertainties are noted as some technologies are yet to be proven commercially and applied in B.C. All four systems offer multiple improvements over today’s conventional netpen production systems, however each system offers different advantages and disadvantages in terms of environmental, social, and economic performance. Land-based RAS and hybrid systems are the two technologies ready for commercial development in B.C., while floating closed containment requires 2-5 years of further review, and offshore technologies may require 5 to 10 years of review.

Development path in British Columbia

Several things need to be aligned in order to promote innovation in Canada and to position B.C.’s salmon aquaculture sector for growing global seafood export opportunities. In general, national legislation and policy needs to clarify the requirements for aquaculture in terms of environmental and social performance and this will send the appropriate signals for investors to develop the technologies that meet the challenge. There are other requirements specific to each of the four production systems and these are discussed in order to attract and stimulate industry investment.

Incentives to build innovation in Canada

A number of measures are suggested for nurturing innovation based on what has taken place in other countries that are leading technology advancements. Some examples are development licenses with reduced fees, marine sites with biomass allocations for innovative technologies, guaranteed loans, accelerated capital depreciation, along with research and development funding models that combine industry, government, and academia contributions.

1 Introduction

1.1 Background

There is strong interest from government, industry, non-government organizations and Indigenous peoples to accelerate the adoption of salmon aquaculture technology that minimizes environmental impacts in British Columbia, while supporting rural economic development, employment, and the security of Canada’s food supply.

This interest extends beyond the province and is shared internationally across salmon producing countries. There are two primary drivers of new salmon production technologies, namely:

- pressures from governments and stakeholders to adopt more environmentally friendly technologies

- challenges such as sea lice and algal blooms that affect salmon production

The industry has largely focused on improvements to conventional marine netpen systems to improve environmental performance while maintaining operational and financial feasibility, but new alternative production system technologies are now advancing rapidly.

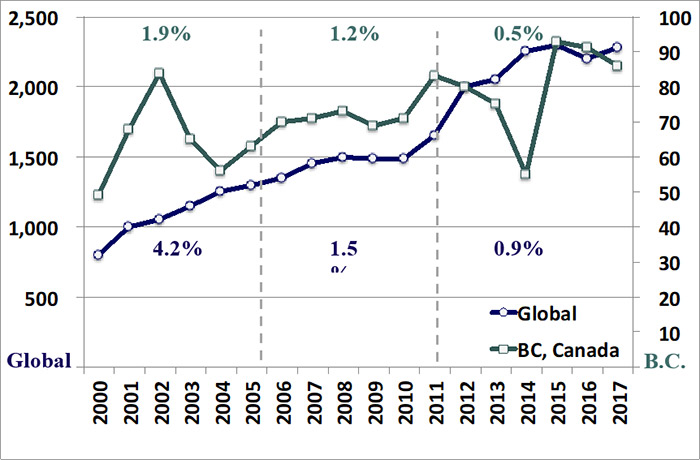

As concerns with conventional netpen systems were not fully addressed, expansion of salmon aquaculture slowed in recent years. Since 2000, the average annual growth in production volumes nearly stalled both in B.C. and globally (figure 1) as limited opportunities for conventional aquaculture expansion were available. Space for marine netpens in some jurisdictions are fully utilized and governments have not increased the number of sites or biomass stocking limits at existing sites (for example, New Brunswick). In other jurisdictions there have been moratoriums on allocation of new sites even though space is available, while comprehensive reviews were undertaken to establish new approaches for salmon aquaculture development (for example, Nova Scotia).

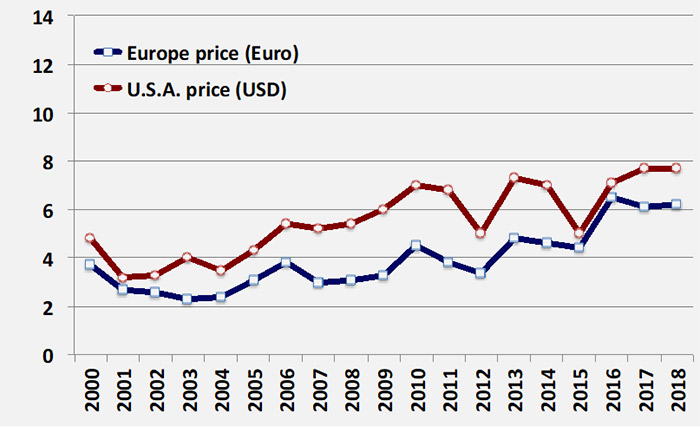

While the pace of growth slowed, demand continued to grow. This bears out in rising prices reflecting the tension between demand and supply of farmed salmon products. Since 2000, prices for major markets including Europe, Chile, and North America have all climbed (figure below).

Two factors continue to apply upward pressure on demand:

- the stagnation in global fisheries catch

- the rising global population including a growing middle class in many countries

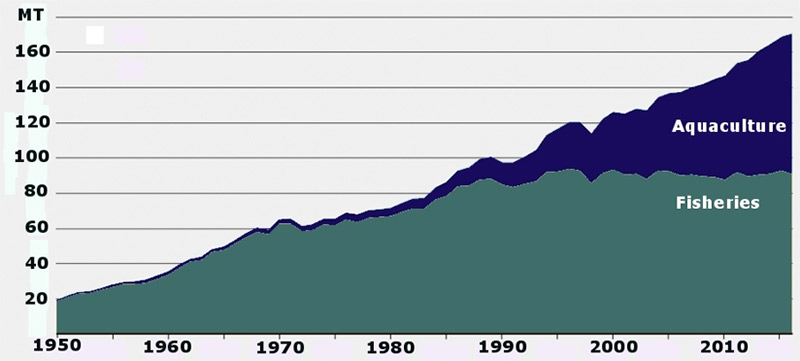

World capture fisheries landings have been flat since the mid-1990s as numerous fisheries reached unsustainable levels (figure 3). There are no near-term prospects for increasing fisheries catches, however aquaculture production (all products) climbed since the 1990s and farmed fish volume surpassed captured fish volume for the first time in 2014 (FAO, 2018). Additionally, the global population is expected to reach nearly 10 billion by 2050 (2 billion more than today; FAO, 2018) and there will be strong demand for aquaculture products as a valuable source of protein.

Canada’s farmed salmon products compete in global commodity markets where prices fluctuate as much as 30% in a year according to supply and demand. Canadian producers must remain competitive and resilient under these market pressures.

This combination of pressures on salmon producers has spurred efforts to develop new technologies for salmon production that address the key issues noted above. The last ten years have seen major steps towards aquaculture production technologies that significantly reduce interactions between aquaculture and the natural environment. Closed-containment systems are of particular interest where, for example in land based systems, most water is continuously treated and re-used. Ocean-based closed containment (that is,, solid walled cages), and open-ocean (offshore) aquaculture systems are also being extensively researched. The use of these production technologies along with innovations such as sensor technologies and data analytics offer reduced environmental impacts for marine environments.

At this critical point in global salmon aquaculture development an assessment of alternative technologies for salmon aquaculture is necessary to advance sustainable economic growth in Canada. Fisheries and Oceans Canada (DFO) in partnership with the Province of British Columbia and Sustainable Development Technology Canada (SDTC) commissioned this study on the global state of salmon production technology with a focus on British Columbia’s (B.C.) operating environment. This will support the aquaculture industry to consider alternative production systems that facilitates expansion of the industry to meet the strong growth and demand for sustainable seafood.

1.2 Indigenous communities

Indigenous communities have a key role to play as new aquaculture technologies develop in British Columbia. Indigenous communities are in an excellent position to participate in aquaculture growth due to their aquatic resources, rights, and access to suitable aquaculture sites. They are already engaged in every aspect of the salmon farming value chain from hatchery, grow-out, processing, and support services to distribution and marketing. They have also played a central role in new technology developments including the Kuterra land-based RAS project. National aquaculture socio-economic impact estimates indicate that about 10% of all economic activity in Canada is the result of Indigenous participation (GP, 2016). This percentage is higher in B.C. than other parts of Canada, and recent developments support further indigenous participation.

The Government of British Columbia adopted a policy in 2018 whereby, starting in 2022, the Province will grant tenures only to fish farm operators who have negotiated agreements with the First Nation(s) in whose territory they propose to operate. Indigenous communities are also highly engaged in aquaculture as investors, operating partners, and through a growing share of the aquaculture workforce. Indigenous communities are keenly interested in developing sustainable aquaculture production technologies.

1.3 Approach

Global scan

Canadian companies and researchers have participated in major technological developments including some of the first commercial land-based recirculating aquaculture systems (RAS), floating closed-containment systems (CCS), offshore production systems, and a range of sensors, remote operated vehicles, software and other system advancements. Most of these have been smaller isolated developments in Canada and they are not scaling up across the industry as rapidly as in other countries.

Major investments in leading systems at commercial scales are emerging in Norway, Denmark, Poland, China, and the U.S.A. among others. There are different reasons for advancement in each country that involve combinations of: the size of their aquaculture industry, size of consumer markets, constraints on marine netpen production, or supports for innovation in environmental, social, and economic performance. This assessment relies on a scan of global leaders to identify technologies that are emerging for commercial application and approaches that will move salmon technology forward.

Document review

As technology has advanced and the level of interest has risen dramatically, a great deal has been written about alternative production systems. Industry reports, government studies, academic research papers, conference proceedings, and popular press articles all provide a rich foundation of information for this assessment. As the developments are evolving rapidly it has also been helpful to obtain some of the latest information from the companies that are either developing these technologies or purchasing them.

Interviews

In order to fully appreciate the information and delve into key issues, including advantages and disadvantages of technologies, it is necessary to speak with many key informants. Private sector, public sector, academic, and non-government organization representatives have all helped to inform this assessment. This is particularly helpful with respect to understanding how technologies that are being developed elsewhere should be considered for applicability in B.C.

Evolving technologies

It must be recognized that while this assessment can only reflect a point in time, aquaculture technologies are developing very rapidly. The relevance of similar assessments completed just five years ago is limited. Much of the information about the performance and capabilities of aquaculture systems quickly becomes outdated. The scale of commercial designs increase, capital costs per unit of salmon produced are dropping. The costs associated with new technologies are also dropping as demand increases and designs are standardized to produce modular “off the shelf” products. There are often annual improvements in the efficiency, reliability, and environmental performance of systems. This trend will continue over the next five years and beyond. This means that decision-making criteria such as environmental performance requirements can remain constant, but flexible, will allow for the ongoing evolution of systems and the arrival of other new technologies.

2 Scope of assessment

2.1 Production systems considered

In January 2018, the B.C. Minister of Agriculture’s Advisory Council on Finfish Aquaculture (MAACFA) Final Report made the following recommendation (5.2):

“Conduct a study examining the feasibility of utilizing closed containment technology in B.C. (land-based recirculating aquaculture systems, advanced net-pen systems, near-shore floating containment and off-shore farming systems) as (i) an alternative to ocean-based open net-pens and (ii) an option for expanding the current salmon farming production.”

This report builds on that recommendation, specifically by assessing the following four broad production systems:

- land-based recirculating aquaculture systems (RAS) for market salmon

- hybrid systems combining land RAS production of post-smolts with marine grow-out to market size

- floating closed-containment systems (CCS) to produce market salmon

- offshore systems involving open or closed containment systems

There is also discussion of supporting technologies such as sensors, artificial intelligence, remote operated vehicles, and other developments that generally support advancements in all of these main production systems.

In order to consider the advantages and disadvantages that the four production technologies offer, the analysis relies on certain assumptions to make systems comparable.

- market size salmon

- All four systems are assumed to produce the same average size of market salmon (about 5kg).

- commercial scale production

- All systems must offer production capacity that is typically used by companies today (about 3,000 mt) and by arranging modular arrays and multiple sites the technology could be used to meet most or all of British Columbia’s current volume outputs.

- steady-state analysis

- The analysis primarily focuses on a future steady state of operations for each technology. This is consistent with a number of the recent international studies on new technologies. In places, the construction and installation impacts are discussed to appreciate key differences between technologies.

- biomass limits for existing netpens

- The maximum biomass allowed for hybrid systems using marine netpens at current aquaculture sites is assumed to remain the same, although increases for semi-closed and offshore systems may be allowed based on meeting environmental performance requirements.

Before describing the new technologies in more detail, it is helpful to illustrate what environments they are being designed for (figure below). Most of the environmental concerns relate to inshore sheltered marine ecosystems where wild salmon migration routes exist, are more concentrated and the opportunity for disease transfer are more pronounced. These inshore waters tend to be more shallow with weaker currents and lower rates of water exchange, so waste and effluent from aquaculture is more likely to build up and cause problems. The other technologies consider other location alternatives including land, inshore exposed sites or offshore sites. It has been easiest and cheapest to start developing aquaculture in sheltered inshore locations, but technology advancements now offer capabilities for operation in the other environments.

The most developed new technologies are designed for land and sheltered inshore environments. These new technologies have been operating at commercial scales for several years and “off the shelf” systems are more readily available. Inshore exposed systems and offshore systems are operating at commercial scales, but these have been deployed more recently and are expected to be refined in the next three to five years.

Currently about 98% of global salmon production comes from open netpen systems in sheltered and exposed in-shore environments (about 94% of B.C. total). The advancements this study focuses on are:

- Closed containment

- using a barrier added to the containment system to stop transfer of diseases and pathogens, waste effluent, salmon escapes and other wildlife interactions. Water is pumped through the system and may be filtered before supply to the salmon, while waste is removed from outflows for processing on land.

- Semi-closed containment

- using a barrier that does not remove all waste from system outflows, but reduces diseases such as sea lice.

- Submersible

- systems may be open or closed with submersible capabilities to help avoid sea lice problems that occur near the surface, and to help access better growing conditions at greater depths (for example, cooler water in summer). These also avoid storm damage and reduce salmon escapes.

- Offshore systems

- are mostly open although some re-purposed marine vessels offer full containment that can be moved to offshore locations.

Many of the distinctions between new technologies are related to the grow-out stage of the cycle, and appreciating the implications of this will help to understand the assessment findings later in this report. The following stage sizes and growth periods are based on data from Kuterra research and insights provided by other salmon farming experts:

- Smolts are produced in freshwater land-based hatcheries regardless of the technologies that are used to bring salmon to market. Smoltification is when salmon change lifestages from being “parr” in freshwater to “smolts” adapted to saltwater, and this is induced in salmon hatcheries by controlling the amount of light salmon are given each day. This is now commonly done when the salmon reach about 100 to 150g after 8 to 10 months.

- Larger smolts and post-smolts are becoming more common and growers in B.C. are already expanding the use of land-based RAS to grow salmon larger before transferring them to sea. Globally the potential size ranges from 200g to 1kg or more before they are transferred to new technologies for on-growing, or remain in land based RAS to reach market size. Having said this, most of the focus is on larger smolts in the 200g to 500g range, with the aim of keeping the on-growing period to a year or less. The growth from 120g to 1 kg takes about 5 to 7 months. Since the optimal size for specific technologies and growth plans is still to be determined, there is a wide range of possibilities for this growth stage. This phase is most likely to be carried out in land-based RAS facilities, but may also be carried out by other technologies, especially floating CCS. For this report it is assumed to be carried out in land-based RAS, and grow out to market size is where different technologies are used.

- Grow-out to market size will take salmon from between 200g and 1kg to an average size in the range of 5kg to 6kg. The time needed to grow from 1kg to the 5 to 6kg range is about 9 to 12 months. The time frame will depend on the target harvest size, and starting at 250g will likely require the full 12 months while starting at 1kg will take closer to 9 months. Being able to keep the grow-out period short will be important for harvest rotations, and flexibility in the timing of transfer to new technologies. Also recognize that the salmon requires greater volumes of high quality water as it grows, and this has implications for the capital and operational costs of different technologies at this stage. For instance, a high proportion of closed containment systems investment is for larger tanks, pumps, and filtration systems needed to meet these grow-out needs, whereas marine systems largely rely on natural water flows and ecosystem services to provide these. In land-based systems the costs are borne by the producer, whereas in open marine systems the “costs” are external to the producer and may be borne by the public or other marine resource users.

2.2 Land-based RAS grow-out

Land-based RAS involves growing salmon in tanks on land in closed buildings to maintain an environment that is highly controlled and secure. The water intake is treated with ultraviolet light or passed through special filters to prevent disease and contamination that could affect fish health. Upwards of 99% of the water is re-circulated on each cycle through the system. Waste material (for example, faeces and excess feed) is removed from the water (for example, drum filters), and depending on the contents of the material (for example, salt) may be suitable for composting, supporting aquaponics (adjacent crop production), or producing energy in connected biodigesters. The water is then passed through bio-filters (bacteria living in sand or plastic media) to convert harmful ammonia generated by the fish into acceptable nitrate form. Aeration is used to drive out carbon dioxide generated by the fish, and oxygen is added to the water before re-circulation. Land-based recirculating aquaculture systems (RAS) have been used for decades in the production of salmon smolts (for example, 75 to 100g). RAS designs have been used for an even longer period for producing a wide variety of other fish species. In the last five to ten years these systems have advanced to successfully produce market-size salmon (for example, 4 to 6kg).

Some systems have produced up to 1,000 mt of salmon annually, but systems being constructed now tend to be 3,000 mt or more to achieve better financial returns. High capital costs have led to larger facilities being built to gain efficiencies of scale. The larger facilities employ modular designs to reduce risks associated with component failures or contamination events. The list in the table below is only a small selection of land-based RAS developments since there are now over 50 operating, under-construction, or approved, although not designed for market-size Atlantic salmon production.

| Status | Company | Location | Capacity (mt) |

|---|---|---|---|

| 7 years prod | Shandong Oriental | China | 2,000 |

| 6 years prod | Danish Salmon | Demark | 2,000 |

| 6 years prod | Atlantic Sapphire | Denmark | 700 |

| 3 years prod | Global Fish/Pure Salmon | Poland | 600+ |

| 4 years prod | Kuterra | Canada | 370 |

| 4 years prod | Sustainable Blue | Canada | 500 |

| Construction | Atlantic Sapphire | USA | 30,000+ |

| Construction | Whole Oceans | USA | 50,000 |

| Construction | Nordic Aquafarms | USA | 33,000+ |

Sources: UnderCurrentNews, 2019; FishFarmingExpert, 2019; company websites.

The initial proposed scale for the Atlantic Sapphire facility in Miami, Florida was 30,000 mt with a phased approach to reach 90,000 mt. The plan for 2030 was just increased to 220,000 mt in an announcement May 8, 2019. This level of production would supply more than half of the current salmon market in the U.S. The projected scale is still highly speculative since the site has not completed a production cycle at this time. Some operators have revised their capacity expectations (for example, Danish Salmon) as they have not been able to reach initial estimates.

System requirements

- Coastal resources

- The versatility of land based RAS systems are facilitating salmon production in other countries with warmer climates including desert conditions (Evans, 2019). Still the need for freshwater and saltwater at temperatures suitable for salmon (for example, 14 Deg C) means that coastal areas like those found in B.C. are ideal. A couple years may be needed to find the right combination of saltwater, well water, injection wells, transport networks, affordable land, power requirements, and local waste handling requirements. This time frame for siting has been the experience where land-based RAS has been planned and built elsewhere.

- Low-carbon power

- The high rate of water pumping means that grid connected three-phase power is required, so remote sites where some marine netpen operations currently operate would not work. Electricity should be from a low-carbon source such as B.C. Hydro (about 90% hydroelectricity) given global commitments to reduce greenhouse gas emissions and expected increasing costs of fossil-fuel based power with carbon pricing.

- Supply-chain

- This involves proximity to feed mills, fish health scientists, fish processors, equipment supply and maintenance companies, and distribution to consumer markets including excellent connections by road and air. When proximity to consumer markets is cited as an advantage of land based RAS in the U.S., it is usually referring to transport costs from Europe, whereas B.C. products reach the U.S. west coast markets and others quickly and economically.

- Trained workforce

- Producers will need trained workers, and there is currently a shortage globally. Closely tied to this is the need for training programs through universities and colleges in coordination with working land based RAS facilities to provide hands-on experience.

– (Hobson, 2018; G. Robinson pers. comm., 2019)

Remaining challenges

- Fish quality

- Managing the system to avoid off-flavours is an on-going key topic for RAS producers.

- Fish health

- Microbes and bacteria in particular bacteria are being studied in closed system components, salmon tissues, and under certain growing conditions. Other issues include microparasites and water compounds such as sulfides that can reach toxic levels. Control measures including water intake and recirculation filters, construction materials, anti-fouling agents, ozone treatment, and fish waste management are all important areas of research.

- Broodstock development

- This will focus on gender advantages, triploidy, late maturation, tolerance to high stocking density and low oxygen.

- Large tank design

- There is ongoing research to optimize water velocities, placement and design of nozzles, and other measures to achieve proper distribution of oxygenated water and collection of waste in larger tanks of different shapes. This is critical to scaling up facilities.

- Energy efficiency

- Improvements in water pumping, filtration, lighting, heating and cooling, and other system components and functions will continue to gain efficiencies while maximizing fish welfare and performance.

- Feed formulations

- New developments aim to meet sustainability criteria with alternatives to fish meal/oil ingredients that are suited to land based RAS needs including efficient waste collection. For these systems this must not hinder biofilter function or off-flavours.

- Stocking densities

- This affects water flows in tanks, fish health and welfare, revenues, loads on recirculation system components.

- Design and construction efficiency

- Given the high impact of capital costs on the viability of these systems, there will be continued efforts to find more cost-effective designs and construction techniques.

- Financial risks

- The projected addition of global salmon production due to land based RAS and other technologies is expected to bring prices down as the tension between supply and demand is alleviated (Gibson, 2019). Depending on the severity of price drops, land based RAS profitability may be affected. This market risk, coupled with production risks, will drive efforts to reduce land based RAS costs and build a stable track record to satisfy investors and insurance companies.

(Summerfelt, 2018; Føre et al, 2018; CtrlAqua, 2018; Aspmark, 2018).

2.3 Hybrid systems with land-based and marine sites

Land-based RAS technologies are being developed for use in combination with marine grow-out sites (that is, hybrid approach). The hybrid approach involves producing post-smolts weighing from 250g to 1kg. The land-based portion provides better growing conditions and reduces early growth phase risks at sea. The shortened grow-out period reduces some environmental risks at marine sites and avoids the most costly portion of land-based systems in the grow-out phase. The grow-out stage in land-based RAS systems requires substantially more capacity that increases capital and operating costs. Current hybrid technology development is focused on finding the appropriate size of post-smolts for transfer to sea as a number of factors are considered in order to optimize the use of the land and marine production systems. Regardless, the aim is to have salmon in the marine environment for at most one year instead of the typical two years for full marine production. Grow-out could involve floating closed-containment in near-shore environments or offshore production technologies, but the near-term focus is on utilizing netpen technologies at nearshore marine sites. Some examples of netpen technology innovations that help address environmental issues include: automated feeding systems integrated with sensors and machine learning to reduce waste, replacement of antifouling chemicals by high pressure seawater cleaning of netpens, improved materials for nets to avoid escapes and increase water flow through the system, and use of underwater remote operated vehicles (ROV) and robots for a variety of tasks. Sea-lice are a particular focus with developments involving: sea lice vaccines, anti-sea lice skirts, “snorkel” nets that keep salmon below sea-lice in the water column while allowing salmon to reach the surface for air-intake, sea lice detection and monitoring of individual fish, cleaner fish, wellboats coupled with CleanTreat technologies that cleanse the water effluent after treatments, as well as ultrasound and resonator treatments (BCSFA, 2018). The table below is a small selection of global hybrid technology developments.

| Salmon size | Company | Location | Capacity (mt) |

|---|---|---|---|

| 150g+ | Grieg | Adamselv, Norway | 1,600 |

| 250g | Norway Royal Salmon | Hasvik, Norway | 2,000 |

| 500g | Bakkafrost | Faroe Islands | 7,000 |

| 650g | Mowi | Faroe Islands | 1,000 |

| 500g | Leroy Seafood Group | Hordaland, Norway | 4,000 |

| 700g | Salmones Magallanes | Chile | Expansion |

| 150g | Mowi | B.C., Canada | 1,000 |

| 300g | Cooke Aquaculture | NB, Canada | Planned |

Sources: UnderCurrentNews, 2019; HatcheryInternational, 2019; company websites.

System requirements

- Land-based requirements

- This portion of the production cycle in hybrid systems has some requirements equivalent to those already discussed for land-based systems. Keep in mind production of post-smolts generally requires saltwater but not in the Faroe Islands, for example, so water intake and discharge requirements may lead to different facility locations (adjacent to the sea rather than inland) compared to some land-based RAS hatcheries that are using freshwater only. Locating adjacent to the sea and near grow-out sites will also be needed for optimal transfer of salmon.

- Transfer to marine sites

- This will be similar to conventional transfers today, however stress of fish at larger sizes is being studied to optimize procedures.New larger vessels (not only for transfers) are being designed to service marine sites and coastal infrastructure must be developed to support these.

- Marine requirements

- Hybrid post-smolt system requirements are similar to existing netpen requirements. Depending on the regulatory limits for biomass by site and/or bay area, availability of sufficient sites to rotate stocking of larger post-smolts will require new production planning, and this can be accommodated in B.C.

Research challenges

Research challenges identified in the previous land-based RAS are applicable for the hybrid system, although less pronounced since the hybrid approach does not need to bring salmon to market size on land. Land-based RAS hatcheries are already very experienced in producing smolts of about 150g for marine net-pen grow-out today, so hybrid systems need to extend this in the range of 200g to 500g or more and successfully transfer these to sea. Grieg Seafood in Norway put 400g smolts to sea in 2018 and harvested 6kg average salmon after 11 months (F. Mathisen pers. comm., 2019). Some of the specific hybrid system challenges are as follows:

- Transfers

- The transferof fish from land to marine sites can cause stress to fish and research is focused on determining the best conditions (for example, temperature, salinity, feeding, fish size, and genetics) as well as new handling systems for low-stress transfers.

- Sea lice

- The use of marine netpens for grow-out willcontinue to require methods for addressing sea lice, although the sealice presence and outbreak risks are greatly reduced with larger post-smolts spending less time in the marine environment. Addressing sea lice is not only a requirement for operation of marine sites, but it helps avoid reduced harvest sizes and revenues. The cost of sea lice management may continue to climb as resistance, fish welfare, and treatment effects on the environment drive investigation of more expensive alternatives. The use of skirts (additional barriers outside netpens) and other measures will continue to evolve for better protection against sea lice and wildlife interactions.

- Algal blooms

- (Heterosigma algae) may persist as a problem for open netpens. Although insurance can cover some loses, this ultimately comes at a cost to operators.Oxygenation and aeration diffusers for structured upwelling (also to prevent sea lice) are promising to be effective for algal blooms.

- Other environmental impacts

- Wildlife interactions, escapes, waste effluent, and other environmental issues associated with marine netpen sites will continue to be a focus of research efforts.

- (Aspmark, 2018; Bjorndal and Tusvik, 2017)

2.4 Floating closed-containment systems (CCS)

Floating closed-containment systems (CCS) offer some advantages of closed systems while retaining some benefits of growing in a marine environment. There are design variations with solid or flexible wall construction, and mechanisms for collection of waste materials. The main advantages of this system include collection of most feed and faeces waste, cost-effective use of surrounding waters, and barriers to: diseases, parasites, wildlife interactions, and escapes. The growth and survival of salmon using floating CCS has been superior to open netpen systems, and there have been no sea lice issues. These are more suitable to sheltered sites in lower energy environments, but some are capable of operating in more exposed locations. Most systems are fixed, but mobile versions using new or retrofitted marine vessels also meet floating containment criteria. All systems involve pumping water from sufficient depths (for example, 12m or deeper) to address sea lice, algae, temperature regulation and other requirements. In most operational systems, the smolts from land-based systems are transferred to the floating CCS system for post-smolt production (1 to 2kg), then grow-out to market-size occurs in open systems. However, some are now being used to grow salmon to full market size (for example, Neptune system). Cermaq plans to bring a system into B.C. operations this year to produce 2kg post-smolts in a flexible wall system. The Hauge Aqua designed “egg” technology, purchased by Marine Harvest and granted development licences in Norway, may be stocked this year. It offers a surface cover for complete enclosure, water filtration system, water intake from depth to avoid sea lice, waste collection system, and a unique feeding system that improves food conversion.

The capacity of most systems ranges from about 225 to 1,000 mt per tank and these can be combined in arrays to produce larger volumes. The concepts involving rebuilt ships currently produce about 300 mt, but are poised to become much larger and may eventually exceed 4,500 mt. The assessment (later in this report) will focus on using these for market grow-out, but these are likely to be integrated with existing open netpen arrays as an intermediate step (that is, post-smolt growth).

| Status | Company | Location | Capacity (mt) |

|---|---|---|---|

| 5 years prod (PS) | Aquafarm Equipment | Norway | 1,000+ per tank |

| 7 years prod (MS) | AkvaFuture | Norway | 1,000+ per tank |

| 7 years prod (MS) | AgriMarineFootnote 1 | Canada | 1,000+ per tank |

| 4 years prod (PS) | Preline | Norway | 300 per vessel |

| Testing (MS) | Hauge Aqua | Norway | 1,000 per egg |

| Testing (MS) | Botngaard System | Norway | 400 |

| Testing (MS) | Seafarm Systems | Norway | 1,000 |

Sources: UnderCurrentNews, 2019; FishFarmingExpert, 2019; company websites. PS=Post-smolt production, MS=Market-size production

System requirements

- Coastal resources

- These must be located in sheltered coastal areas with access to suitable saltwater environments (for example, temperature, currents, water quality). There is somewhat greater flexibility in sites compared to open netpens since warmer locations can be accommodated by pumping cool water from below the tank and sites prone to algal blooms may still be acceptable. Some land may be needed for processing waste materials.

- Power source

- Grid-connected three-phase power is needed, so remote sites where marine netpen operations currently run on diesel would not meet requirements. Electricity should be from a low-carbon source given global commitments to reduce greenhouse gas emissions.

- Supply-chain and access

- Connection to feed (inputs) and consumer market (outputs) requires excellent connection by road and/or air.

Remaining challenges

- Waste disposal

- Technologies for separating waste from water outflows will continue to improve. Research will seek to increase the amount of solids captured, minimize the amount of dissolved nutrients (for example, nitrogen and phosphorus), and develop ways of processing and utilizing the waste materials on land.

- Water flow and tank size

- There is ongoing research to optimize pumping of water through tanks of different shapes and larger sizes. Current floating CCS tank designs tend to be smaller than industry would like for commercial operation so this challenge must be addressed.

- Structural design

- Materials used to build floating CCS tanks will be explored for rigid and flexible options. The shape and size of tanks as well as walkways, platforms, and other functional components will develop.

- Market-sized salmon

- There is more floating CCS experience with post-smolt production and market-size for other species, and efforts now focus on refining approaches for market-sized Atlantic salmon production. - (Føre et al, 2018).

2.5 Offshore systems

Offshore systems were tested in Canada in the late 1990s with the launch of Ocean Spar cages in New Brunswick and Norwegian designs deployed in B.C. (Ryan, 2004). Early designs did not sustain commercial production and many improvements have been made globally since. Producers in the Faroe Islands have been leaders in contending with harsh marine conditions, and Ireland producers moved further from the coast in response to strong local opposition to near-shore developments. In the last two years most attention has focused on Norway and China where innovation has rapidly accelerated in response to supportive policies.

There are diverse concepts for offshore salmon aquaculture that each have merits for meeting certain offshore applications. The variety of designs include open and semi-closed systems, floating and submersible options, as well as fixed and mobile systems. Although definitions of offshore environments are somewhat fluid, all designs are meant to operate in minimum water depths of 20 metres and minimum wave heights of 1 metre. In the B.C. context much deeper waters (100 to 200m) and higher waves (at least over 3m and often over 6m) will be common and systems must operate through extreme events. The design of the structure that contains salmon is central, but equally critical is the design and logistics for servicing the more remote sites. Some designs include living arrangements for staff, while others rely on full automation so that workers are not required for day-to-day operations. Transportation to and from the site and land-side infrastructure are important as the challenges are greater for offshore production.

The SalMars Ocean Farm 1 holds about 6,500 mt and may be doubled in size.

Ocean Farm 1, is mid-way through its year-long trial period, and is reporting good growth rates and low mortality (FAO, 2019). The Nordlaks Havfarm 1 is likely to be the world’s longest vessel at 430 metres and capacity for 10,000 mt of salmon. Ramsden (2019) reported that MOWI’s application for development licences in Norway was approved for its offshore “Blue Revolution Centre” research station and two offshore production technology designs – the “egg” and the “donut” concepts. Today’s designs differ greatly and after a few years of operational experience companies will settle on preferred options. Once that occurs many more could be built with the view that salmon aquaculture industry growth will capitalize on the abundance of space available.

| Status | Company | Location | Capacity (mt) |

|---|---|---|---|

| 2 years oper | SalMar owned | Norway | 6,500 |

| 1 year oper | Rizhao Wanzefeng Fisheries | China | 1,000 |

| <1 year oper | Midt-Norsk Havbruk owned | Norway | 1,000 |

| 2019 start | De Maas design | China | 3,750 |

| 2020 start | Norway Royal Salmon owned | Norway | 3,000 |

| 2020 start | Nordlaks owned | Norway | 10,000 |

Sources: UnderCurrentNews, 2019; FishFarmingExpert, 2019; company websites.

System requirements

- Offshore locations

- These must be free of conflicts with other marine users including marine transport, protected areas, fisheries, oil and gas, and other resource extraction developments. In many countries these can represent constraints, but coastal B.C. offers many options.

- Water quality

- This requires suitable temperature profile and currents, while remaining free of contaminants and fish health threats.

- Transport access

- Ideal sites are within 25 nautical miles with reliable year-round navigation between on-shore and off-shore infrastructure. Floating ice and major storms (for example, hurricanes and typhoons) can be limitations in parts of some countries, but extensive areas off the B.C. coast are suitable.

- Proximity

- Minimizing transport for supply-chain inputs (that is, feed mills and aquaculture goods and services suppliers) and outputs (ie. processing and distribution to markets) is important.

- (CEA, 2018)

Remaining challenges

- Autonomous systems

- This system must incorporate technologies to become less dependent on labour for feeding, monitoring, mortality collection, net cleaning and repair among other regular functions. Guidance, navigation, and control of remote operated vehicles (ROVs) and autonomous underwater vehicles (AUVs) are the subjects of intense research for offshore aquaculture.

- Remote power

- Research is focused on production systems that integrate solar, wind, wave or water current energy to power pumps, sensor, robotics, and submersible functions are needed to run autonomous offshore systems.

- Monitoring and decision-support

- to maintain structure integrity and fish heath in the face of challenging conditions including storms. These must be robust and capable of assessing whole farm conditions to drive scheduling and performance of key operations.

- Structure design

- Efforts are focused on flexible and rigid components that provide functionality and security at remote locations. This also involves alternate shapes that are less vulnerable to offshore conditions, and technologies that allow submersible systems to avoid storms and still meet fish health and performance requirements.

- Vessel design

- Well-boats that carry live fish, feed supply vessels, and service boats for fish treatments and structure maintenance are all being purpose-built. These must meet more rigorous standards for safety and functionality to handle the wider range of environmental conditions while maintaining safety of structures and personnel. Research is examining the size and shape of vessels, connections (for example, cranes, hoses, platforms) with offshore aquaculture structures, and dynamic positioning capabilities for vessels to hold their position relative to the structures. Some of this technology is adapted from marine transport, oil and gas, and other marine applications.

- Safety

- must be met according to occupational health and safety laws, which are not necessarily developed for offshore aquaculture. For instance, the Atlantic Offshore Health and Safety Regulations are developed under the Canada Labour Code with a focus on oil and gas activities. These specify requirements for training and education of personnel, certification of systems and equipment, risk assessment plans, monitoring and controls, record-keeping, passenger transit, fall protection, diving safety, and other requirements must be devised for offshore aquaculture.

- Fish health

- key factors in offshore environments must be better understood. Stocking, feeding, treatment of diseases and parasites must be designed for this environment involving stronger currents and larger waves.

- Wildlife interactions

- Unlike near-shore environments where most aquaculture production experience exists today, the offshore environment has different marine mammals and predators and there is a need to understand how they will interact with these systems, especially as they become larger and more numerous.

- Regulatory uncertainty

- Pilot testing will help regulators to understand and monitor these systems then develop appropriate regulatory frameworks. Key questions involve site ownership, who will grant approvals, the application process and requirements to be met.

- (Exposed, 2018; Bjelland et al., 2015, Fard and Tedeschi, 2018; NRCan, 2018; Holmen et al., 2017)

2.6 Supportive technologies

There are a wide range of technologies with cross-cutting benefits for all four alternative production systems. These technologies are not formally assessed according to environmental, social, and economic criteria, but they are expected to improve performance across the board. Some of the most promising recent developments are described briefly in turn below and a few Canadian opportunities are highlighted.

- Sensors and control systems

- Traditional data collection from monitoring and diagnostics is all being digitalized and analyzed in real-time for timely management decisions. Temperature measures, carbon dioxide and dissolved oxygen readings, video recordings, signs of disease, stress indicators, and many other important data feedbacks from the growing environment are captured from growing sites and monitored at data centres. This allows quick recognition of issues and faster response times. “Big data” can also be used to determine trends, identify drivers of performance, support decision-making, and link biological measures with economic performance. Sensors, feed systems, and computers are being linked by wireless networks building the Internet of Things for aquaculture production. Some data is already available on mobile devices so managers can monitor from anywhere. Software to integrate systems and employ artificial intelligence is leading to automatic decision-making by advanced production systems. Many companies are contributing elements and some are developing packaged integrated solutions.

- “Intelligent” farming

- Sensors and data analysis are being combined to deliver individualized farming for fish. This can lead to precise feeding and treatments for each fish based on fish health and a suite of measurements. BioSort and Cermaq have combined efforts to develop iFarm that uses recognition of spot patterns and other morphological features to identify individual fish and track their health. For example, instead of treating all fish for sea lice, only the individuals that meet thresholds will be treated. This type of technology avoids over- and under-feeding each fish, and individual fish can be selected for harvest based on size and availability.

- Feed innovation

- Feed suppliers must continually develop products that meet the changing needs of new production systems. Feed formulations are designed for certain health benefits to address diseases, diets for extreme environmental conditions, and to include novel ingredients such as immunostimulants, antioxidants, or metabolic stimulants. Feeds are developed for increased efficiency (that is, feed conversion), better quality control, and more sustainable supply chains. Canada’s largest feed suppliers including Skretting (offices in Saint Andrew’s, NB and Vancouver, B.C.), and Corey Aquafeeds (Fredericton, NB), remain at the forefront of feed research and they supply feed to clients all over the world.

- Transport and logistics

- Marine vessels and containers are increasingly specialized for new production systems. Advanced positioning systems and cranes are being developed in parallel with the needs of new vessels. Work-boats and well-boats are equipped with fish handling and treatment capabilities, and harvest ships are being developed with on-board processing so salmon are ready for market by the time they return to shore. Other vessels are being specially designed for exposed and offshore locations including the Arctic. The international firm AKVA group (satellite office in St. George, New Brunswick) is delivering a barge to Arctic Offshore Farming (Norway Royal Salmon) to use above the Polar Circle. It can operate in 7.5 metre waves and has 800 tonnes of feed capacity for supplying submersible production systems. Canada has a number of ship and boat building companies that have extensive experience customizing designs for specialized applications.

- Nets and mooring

- As production systems move to exposed and offshore environments there is a need for innovation in containment materials (for example, steel, HPDE, Dynema, AquaGrid and other nets). These offer strength, rigidity, reduced risk of escapes, reduced antifouling and maintenance, and suitability for integrating monitoring systems. Mooring equipment may come in flexible and rigid forms and it is critical to reduce risks associated with metal fatigue and corrosion, as well as component failure that could lead to potential system failure. Companies are developing products made of lighter-weight materials, with increased lifespans, faster installation, and certification to international standards. Based in Campbell River, B.C., Poseidon OceanSystems is a supplier of these products and spends close to half of staff time on research and development, resulting in over a dozen product innovations and four (4) patents in recent years.

- Robotics

- Semi – to fully automatic robots as well as remote operated vehicles (ROVs) now perform a number of previously difficult and costly tasks. Inspection of nets and moorings for damage has traditionally been done by divers, but dive time and safety precautions make this a challenge. Cleaning and repair of nets and other components can be done by robots, along with sample collection and analysis from sediments below nets or inside containment structures.

- Specialized broodstock

- It is becoming more important to develop salmon with certain high performance characteristics for new systems. Key characteristics include gender, late maturation, tolerance to less oxygen, survival in high energy environments (for example, offshore), among others. Canadian salmon producers, universities, Genome Canada (B.C. and Atlantic centres), and private research firms are engaged in these developments.

3 Sustainable aquaculture technology criteria

3.1 Technology assessment

Innovation in aquaculture aims to improve upon the performance of current production systems and ultimately the success of farm operators. Innovations may improve private and public outcomes of salmon farming operations. Improvements in private outcomes include better designs that lead to lower capital or operating costs, and improvements that gain more revenue through higher quantity and quality of products. Improvements in public outcomes may result from system designs that reduce waste released to the environment, avoid impacts to other wild organisms, minimize energy usage and greenhouse gas emissions, and provide more social and economic benefits to society.

Each of the four production systems that are profiled in this report are assessed according to a suite of criteria grouped into environmental, social, and economic themes. The criteria are considered important to assess since these relate to the primary issues associated with salmon aquaculture production to date. There is no order of importance to the criteria, none is assigned more weight than another, and these are all considered priorities for new technologies to address. After the criteria are briefly described below, the strengths and weakness of the four production systems will be assessed in terms of these criteria.

The assessment is forward looking since these are relatively new production systems that have yet to be widely adopted. As for all outlooks on new technologies there is some uncertainty regarding their performance at large scales and over the long-term. Aspects of the four production technologies that are subject to greater uncertainty and risk will be noted. It must be recognized that there are numerous designs and aquaculture sites for each of the four production systems and these will all have somewhat different performance capabilities, so the assessment is broadly indicative of the expected performance of each production system. Finally, innovation is moving quickly on all four production technologies and this assessment only represents a point in time and this should be reviewed as substantial advancements occur.

3.2 Environmental criteria

There are several key environmental criteria that new technologies aim to meet. The following briefly explains the essence of each criterion so that the benefits of different system capabilities are clear. The first five environmental criteria relate to outputs of salmon production and the last three relate to inputs.

- Marine escapes

- New technologies must avoid salmon escapes from production systems, including escapes during salmon transfer and transport activities. Escaped salmon potentially affect wild salmon populations by competing for food and habitat, and by impacting wild populations through interbreeding.

- Salmon diseases

- Transfer of diseases and pathogens between farmed salmon and wild populations must be avoided. Sea lice is currently the main issue although others are a concern (for example, piscine reovirus, amoebic gill disease), while potentially resistant and new diseases in the future are also important to avoid.

- Waste effluent

- Ecosystem effects of salmon faeces and feed falling to the seafloor must be avoided. These waste deposits cause oxygen depletion in the water as it breaks down and this can both suppress desirable marine organisms and promote undesirable ones (e.g algal blooms). Some commercial fisheries are concerned that effluents can affect the habitat, survival, and productivity of fishery stocks. In land-based RAS systems any saltwater discharge must be be done carefully to protect freshwater and marine resources.

- Chemical release

- Release of harmful chemicals and substances into the marine environment must be avoided. The concerns include anti-fouling agents used to keep cages clean, chemicals used in the treatment of diseases, and feed ingredients. As these disperse in the environment, they can negatively affect other organisms.

- Wildlife interactions

- Interactions with marine predators (for example, seals and sea lions seeking salmon for food) as well as seabirds must be avoided. Wildlife can affect the farm structures and even the farmed salmon, or they may be killed by operators following protocols to protect their farm structures and stocks.

- Water usage

- Unsustainable use of water must be avoided. The withdrawal or return of wastewater to sensitive sources, especially involving limited freshwater supplies such as aquifers, can deplete valuable water resources over time.

- Energy usage

- High energy intensity must be avoided, especially from carbon-based and non-renewable sources. Renewable energy sources and grid connected electricity from B.C. Hydro (90% hydroelectricity) are best. Atlantic salmon aquaculture requires energy for system construction, operation, and transport of products to and from the site. As efforts to combat climate change accelerate, the energy types and quantities used will be increasingly important considerations. Life-cycle analysis results capturing all aspects of construction, operation, and delivery to market (that is, egg to plate) are the best basis for comparing production technologies.

3.3 Social criteria

Long-standing tensions between salmon aquaculture producers and other interested groups are essential to resolve. Meeting environmental and economic criteria is part of resolving conflicts, but social criteria extend beyond this. Focusing on local, global, and consumer perspectives, the assessment highlights how the use of new technologies can help build support and trust in salmon aquaculture production.

- Local support

- Local people in B.C. concerned about salmon aquaculture include: Indigenous people, other residents near production sites (permanent or seasonal), commercial fishers, recreational fishers, tourism operators, aquaculture employees, and local businesses that benefit from economic development. Local support will generally grow for new technologies that are trusted to deliver the benefits of aquaculture while minimizing the negative impacts. Understanding, engagement, partnership, and transparency in use of new technologies will enhance trust.

- Global support

- Environmental non-government organisations (ENGOs) may have a local presence, but are often working more broadly to improve aquaculture operations nationally and internationally. Closely tied to this are third-party sustainable certifications for aquaculture products such as the: Aquaculture Stewardship Council farmed salmon certification, Global Aquaculture Alliance best aquaculture practices program, Monterey Bay Aquarium Seafood Watch program, and the Canadian General Standards Board organic aquaculture standard. These certifications help the other social objectives (that is, local support and consumer support), as the support of ENGOs can also.

- Consumer support

- B.C. producers ship to over 70 countries, however principal markets are in the U.S. and Canada. Many consumers are price sensitive and not necessarily aware of conventional salmon production issues. Eco-labelling can alert retailers and consumers to choices available, but these have had mixed results (Roheim et al., 2011; Rudd et al., 2011; Hallstein and Villas-Boas, 2013). As production grows using alternative technologies it may be important for access to certain markets including retailers, food service chains, or countries. Consumer perspectives will also evolve as more production from alternative technologies comes online and these products are no longer limited.

3.4 Economic criteria

New aquaculture technologies will change the economics of salmon production and this has implications for both aquaculture participants and the general public. Aquaculture participants including private companies, indigenous communities, lending institutions, insurance companies, and government will be concerned with financial performance. Local and regional communities, all three levels of government, and the general public will be more concerned with broader economic impacts beyond the interests of aquaculture participants.

- Profitability

- New technologies must be profitable or they will not be (widely) adopted. Profitability is signaled by investor support of new technologies, and ultimately by successful operations that produce profits over several years.

- Capital cost

- Capital costs will shape how quickly new facilities can be built and expanded. Capital costs are also a factor in financial risk (more below).

- Operational cost

- Operational costs will affect long-run financial performance and ability to compete with other technologies and producers in the market.

- Financial risk

- Financial risk will shape the speed and scale of technology adoption. The amount of experience and demonstrated operation of each technology at commercial scale will affect its speed of adoption as well as the profitability expected by investors (that is, risk adjusted rate of return). Some risks can be mitigated with increased capital costs (for example, back-up systems, sensors and alarms), or with operational costs (for example, insurance), while other risks relate to market fluctuations and other factors that can’t be controlled easily.

- Supply chain

- The availability of the necessary supply-chain to support new technologies must be considered in the B.C. context. This includes technology suppliers, construction expertise, operational expertise, system inputs such as feed, energy, fish health testing, processing, marketing and distribution capacity.

- Economy

- There is a public interest to maximize economic benefits in terms of jobs, incomes, community economic development, and tax revenues to governments. New technologies change the quantity and nature of economic benefits depending on system requirements, location, and potential to grow in a competitive global marketplace for salmon products. This report refers to full-time equivalent jobs unless otherwise indicated.

- Expansion

- Each technology offers different opportunities for expansion of production in B.C. and for export of goods and services to other countries.

4 New technology assessment

4.1 Introduction

The strengths, weaknesses, and uncertainties for the four production technologies are assessed according to the environmental, social, and economic criteria in the tables below. More detail regarding the assessments for each criterion follows the tables.

| Land RAS | Hybrid system | Floating CCS | Offshore system |

|---|---|---|---|

| Marine escapes | |||

|

|

|

|

| Wild salmon disease | |||

|

|

|

|

| Waste effluent | |||

|

|

|

|

| Chemical release | |||

|

|

|

|

| Wildlife interactions | |||

|

|

|

|

| Water use | |||

|

|

|

|

| Energy use and GHGs | |||

|

|

|

|

Overall, all four production technologies offer improvements over conventional aquaculture production. There is no system with the best performance across all environmental criteria. Research is needed to complete more reliable assessments of performance expected for floating closed-containment and offshore systems.

Similarly, for social criteria in the next table, each of the four production technologies will improve local, global, and consumer support. Keep in mind that support is not homogenous or unanimous in each group, for example some consumers may support a particular new technology while others oppose it. The assessment aims to capture the general direction of support and what are the key factors to consider.| Land RAS | Hybrid system | Floating CCS | Offshore system |

|---|---|---|---|

| Local support | |||

|

|

|

|

| Global support | |||

|

|

|

|

| Consumer support | |||

|

|

|

|

| Land RAS | Hybrid system |

Floating CCS | Offshore system |

|---|---|---|---|

| Profitability | |||

|

|

|

|

| Capital cost | |||

|

|

|

|

| Operational cost | |||

|

|

|

|

| Financial risk | |||

|

|

|

|

| Supply-chain | |||

|

|

|

|

| Economy | |||

|

|

|

|

Expansion |

|||

|

|

|

|

The combination of readiness for commercial development, likelihood of being profitable, economic impacts, and opportunity for expansion are what determines the financial and economic benefits expected from new technologies. Overall, land-based RAS and hybrid systems are ready for commercial application in B.C., while the others still need five to ten years. Land-RAS though less financially proven offers greater opportunity for expansion as long as this occurs in B.C. The hybrid system is likely more profitable and anchored in B.C., but expansion may meet challenges.

4.2 Land-based RAS grow-out

The following assessment considers the best available land RAS technology, application in B.C., and facilities being built in different B.C. locations.

Environmental criteria

- Marine escapes

- Zero

- Wild salmon disease impacts

- Zero

- Waste effluent

- There are no concerns since this is handled on land with acceptable disposal in more advanced designs including: composting, soil amendments for aquaponics (plant production) linked to the facility, or energy generation using biodigesters. Discharge of saltwater must be done carefully to avoid contamination of freshwater or marine resources, and land-based RAS offers the best potential waste management of the new technologies.

- Wildlife interactions

- Zero

- Chemical release

- Infection with pathogenic or opportunistic microbes is the main concern in these systems, but standard anti-microbial treatments are avoided since they harm the beneficial bacteria used in the bio-filters (denitrifying bacteria). These systems employ some antibiotics for bacteria, formalin for gill parasites, and alternatives such as low dose ozone.

- Water usage

- This is minimal in state of the art re-circulation systems, in fact salmon facilities are already operational in desert environments. There is a caution regarding exceptionally large developments and sites with water limitations or sensitive environments (for example, aquifers). Requirements for a depuration stage to deal with off-flavours before sale to market may also use more water than the rest of the production scale.

- Energy usage

- This depends on system design and location. In general, these systems use more energy in construction and operation than other systems (Ayer and Tyedmers, 2009). This can be partially offset by generating up to 10% of operational energy requirements using biodigestion of waste material, and locating in proximity to both feed sources and consumer markets to reduce transportation energy. Use of solar panels, wind turbines, and low carbon electricity sources can alleviate climate change concerns.

Social criteria

- Local support

- Strong local support will be built on the system’s ability to improve environmental performance across nearly all measures. Protection of wild salmon, addressing concerns in recreational and commercial fisheries, and avoiding other marine spatial conflicts will substantially address the opposition to salmon aquaculture. Depending on how land-based RAS is developed, local direct and indirect economic opportunities may be lost so coastal communities will raise concerns. There has been some local opposition to the recent large proposed facilities in the U.S. on the basis of water resource concerns or potential noise issues.

- Global support

- Land-based RAS systems are expected to meet or exceed sustainability certification requirements.This is a strong indication that global support from environmental organizations will continue. Monterey Bay Aquarium’s Seafood WatchTM lists “worldwide indoor recirculating salmon” grown salmon as their “Best Choice” (MBA, 2019).

- Consumer support

- The acceptability of products from this system is expected to be high since premium prices have been captured in some markets. This does not imply that price premiums will continue, only that it reflects consumer support. The ability to avoid chemicals in feeds and system treatments will appeal to consumers. The assurance of clean water circulating through the system will be an important feature for consumers concerned about pollutants in the marine environment. There have been some historical issues with off-flavours, but these are addressed in modern designs. The issue of fish welfare may yield mixed consumer responses. On the one hand fish welfare is improved with optimal growing conditions and avoidance of potentially stressful treatments for sea lice and other ailments. On the other hand, high biomass density and aggressive fish behavior must be well-managed with transparency to consumers. Some consumers may perceive land-based facilities as an unnatural environment for raising fish and there will be a need for producers to address this.

Economic criteria:

- Profitability

- Announcements of secured funding for numerous large-scale projects has proven that investors are ready to move this system forward even with relatively high risk. There is a concern that failures of these large projects to deliver on promises to investors could hamper the momentum that exists. Given the need to monitor the success in the next few years for the large systems being built, there is still some caution before declaring these are profitable.

- Capital costs

- The capital costs have dropped substantially over the last ten years and are now in the range of $10 to $14 per kg of salmon capacity for systems with 5,000 mt capacity (Bjorndal and Tusvik, 2017). The largest proposed projects today (over 10,0000 mt) are in the $7 to $10 per kg range (AquaMaof, 2019). These figures do not account for production not always meeting capacity, so actual capital costs per kg of salmon produced will be important to confirm going forward. These capital costs include: site preparation, buildings, electrical, concrete work, RAS equipment, and other installations (excluding land). The time required for permitting is related to capital costs. Any complexity and delay of permitting and approvals is a deterrent to development of land-based RAS systems since financial capital is tied up longer. The locations where large projects are going forward took many years to meet all regulatory requirements. This ultimately represents a cost to operate, risk to investors, and challenge to achieve returns on projects.

- Operational cost

- The operational costs are competitive with other systems, especially where optimal growing conditions and system advantages can reduce costs, and reduced transportation exists in ideal locations. The expected production costs per kg of salmon from land based RAS are now about $5 to $6. For B.C. the transport to the U.S. is economical, but shipping to Asian markets may be a competitive challenge with this system, especially as local Atlantic salmon production capacity in Asia is growing rapidly. Taking into account production challenges such as growing salmon to full size and avoiding any system failures, the actual long-term operational cost will be confirmed going forward.

- Financial risk

- Pathogen control, biosecurity, and system component failures are key concerns for investors as mortality incidents can be severe. High rates of early salmon maturation, poor feeding response to husbandry practices, and stocking density issues can also impact growth, quality, and ultimately revenues. Although recent financing success is a strong indicator that risks are being addressed in new systems, along with a considerable amount of research to advance the above noted concerns, this is ultimately confirmed through successful operations over a number of years. The current environment is favourable, with salmon prices above $9 CAD per kg over the last two years, but in 2011 and 2012 prices fell below $7 CAD per kg (22% lower). These systems must demonstrate financial resilience through price volatility, and also in a global production growth environment. As more land-based capacity develops along with other emerging technologies, a higher proportion of product will be able to meet high consumer expectations and this could erode any premiums that are possible.

- Supply-chain

- Most of the supply-chain elements required for this system are available, but land-based RAS does not have the best supply-chain advantages amongst the four technologies considered. System-specific managers must be trained and the expertise for construction and maintenance are being primarily developed in Europe. As large-scale land-based systems are being developed particularly in the U.S., the advantages in B.C. are not sufficient to have already attracted large developments, and supply-chains will now be developing elsewhere.

- Economy

- Advanced skills and expertise are required for most positions in RAS facilities so locations with excellent training and aquaculture industry presence are in a good position. Given the advanced labour requirements, the salaries and wages are attractive for salmon farm workers. However, the location of these systems is very flexible so coastal employment opportunities may be lost as production moves closer to consumer markets and distribution centres. There are also fewer jobs per tonne of salmon produced than most other alternative technologies. Land based RAS systems operating at commercial scale in B.C. are expected to generate about 26 to 30 direct jobs per 1,000 mt of capacity (CounterPoint, 2019). This is only a small decline compared to hybrid or floating CCS, and a bit more than anticipated for offshore systems. The nature of the jobs will be more technical and average salaries will be higher. The most significant consideration is where these jobs are located in B.C. or elsewhere.

- Expansion

- Sites already selected for existing, under-construction, and proposed land-based RAS facilities around the world demonstrate the flexibility in siting this technology. Although there are many considerations for meeting system requirements and optimizing performance, British Columbia offers options for suitable sites. Based on the size of land parcels secured for recent large-scale farms in Maine and Florida, about 32,000 mt of salmon can be produced on about 20 hectares of land (50 acres). Subject to water source availability, all of the current farmed salmon production in B.C. could be accommodated in a combined space of about 60-hectares (150 acres). This does not mean it is a simple matter to identify the best location(s), and a couple years may be required for site selection considering the substantial investments involved.

4.3 Hybrid system

Assessing the performance of this system revolves around the salmon growth stage from about 100g to 500g where land-based RAS is used. Any environmental and financial risks associated with the fish at this stage in the marine environment are addressed by moving to land, and there are some additional benefits in the marine grow-out phase. The following assessment assumes the marine portion utilizes open netpens with some improvements and that the allowable biomass in netpens remains the same. Any other improvements to the marine phase involving closed, submersible, or offshore developments would further address a number of the marine risks.

Environmental criteria

- Marine escapes